Small Banks offer better Terms for Businesses

We know that there are many ways for a small business owner to get the financing they need to start or grow their company. In this article, we focus on lending sources like small banks, large banks, credit unions, and online lenders and show how business owners rate these different funding sources. We explore the question, which lender are small business owners more likely to seek credit from, and from which financial institution are they more likely to receive approval? Studies from Federal Reserve Banks of New York, Atlanta, Boston, Cleveland, Philadelphia, Richmond, and St. Louis show some interesting trends in the success of small banks in the business lending space.

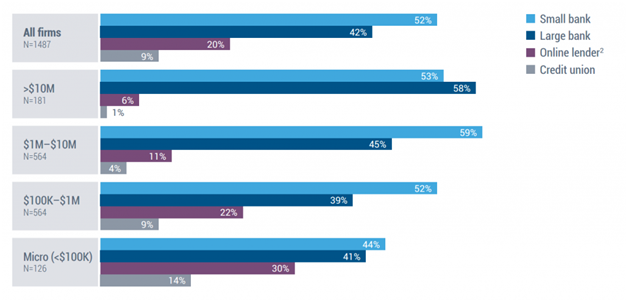

The graph below shows the comparable between the size of the business to the type of institution where the business applied. It is apparent here that small banks make up at least half of all credit sources applied to for nearly every category of company except for micro businesses, which here are defined as businesses with less than $100,000 in yearly revenue. Younger, smaller businesses tend to have more trouble finding financing from banks, which accounts for the accompanying increase in credit unions and online lenders.

(Fundera, 2016)

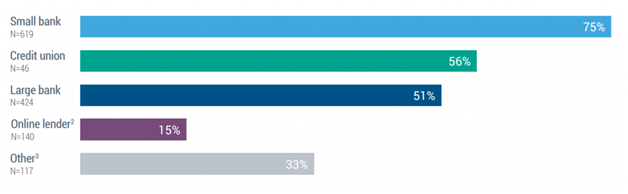

In total, 76% of all applicants who sought credit from a small bank received some funding, while only 58% received funding when they applied to a big bank. The chances of finding successful financing increased alongside the size of the business, and this makes sense, the smaller and younger the business, the more precarious the investment, and banks tend to be risk-averse. That said, though, small banks still out-fund larger banks to a substantial degree at every tier of revenue.

It also appears that business owners were more satisfied with their experience in using smaller banks. Small banks won the popularity contest pretty handily, they were rated as 50% more satisfactory than the runners-up of credit unions and large banks. Small banks still ranked better than big banks everywhere but in the “ease of application process” category and ranked significantly better in the “transparency” category. But again, overall, business owners preferred their small bank experiences much more than their large bank ones.

(Fundera, 2016)

For the year 2015 on the whole, small banks received more applications, funded more small businesses, and were rated more highly per category overall than their lending competition. If you’re a small business owner with more than $100,000 in annual revenue, micro businesses unfortunately still went underfunded in 2015, it seems as though a small bank is the way to go.